Finished Goods Inventory: What It Is, Formula, and Examples

Employers will also conduct graffiti removal, public space maintenance and building restoration. Some employers may use vehicles equipped with high-pressure hot water power washing equipment which is used to remove graffiti or other unwanted surface deposits such as paint, concrete, tar, etc. This classification also applies to the repairing of industrial and commercial chimneys.

- This classification includes the manufacturing of chemical ingredients as well as the blending and mixing of the ingredients.

- Drawing and stiff pattern paper, carbon paper, masking tape, kerosene, H-lead cames (standard, flat and rounded), wire solder and putty are received from others.

- Using inventory management software provides real-time insights into finished goods inventory, enabling businesses to manage stock more effectively.

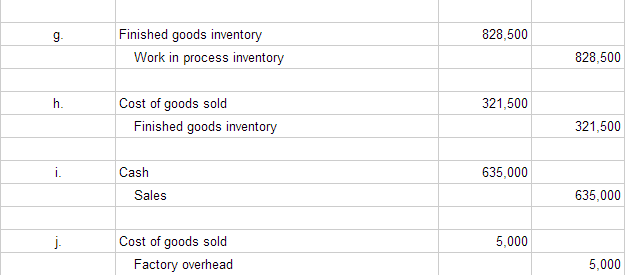

- For example, with the job order costing, the manufacturing company ABC has completed a job with the goods that cost $30,000 during the month.

How to Calculate a Finished Goods Inventory Budget

However, if the goods are fashion items, then their value may decline precipitously as soon as some other fashion trend takes over; this makes them less useful as collateral. Let’s take a deeper dive into how inventory becomes finished goods and how you can make sure your business is fully prepared for sale every step of the way. Let’s look at some examples of how this formula can be applied in real life. Learn to keep customers happy with fast, accurate, and reliable fulfillment.

Finished Goods Inventory: Formula + How To Calculate It

Manufacturers purchasing qualifying machinery, equipment, parts, tools, supplies, or services should use Form ST-121, Exempt Use Certificate, to make these purchases exempt from sales tax. Predominantly means that the machinery or equipment is used more than 50% of the time in a production activity. After the goods have made it through the entire assembly line and are completely ready for sale, they are transferred out of the work in process account to the finished goods inventory account. Overstocking on unpopular designs can lead to dead stock and write-offs.

Cost of Goods Sold: Definition, Formula, Example, and Analysis

This is in linewith the fact that assets should not be overstated, and should only bementioned at the amount at which the company expects to sell them for. The above journal entry can be seen as a baseline case for when the entity is a manufacturing concern. Calculation of the Finished Goods inventory is a very important component for every business, and therefore, it should be calculated properly to give the best results. This is because this is the final stage of their inventory, and it has passed through the previous two inventory stages, which were Raw Material Inventory, and Work In Progress Inventory. Finished goods are considered to have significant value as collateral for a lender, since they can be sold off with no delay for finishing work.

Key Characteristics of Finished Goods Inventory

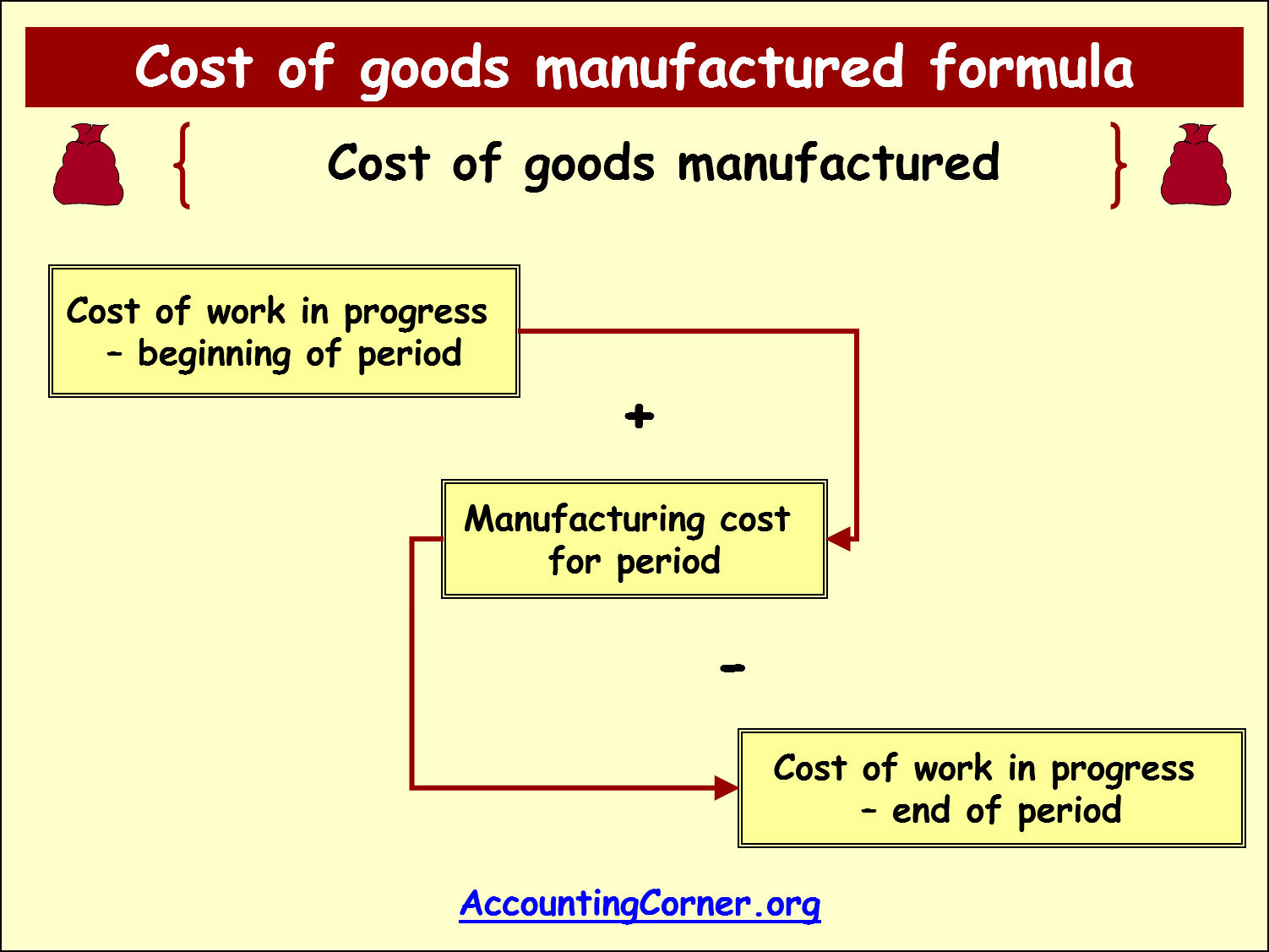

Whether you’re an industry veteran or a newcomer, our easy-to-follow guide will equip you with the knowledge you need to excel in managing your finished goods inventory. While holding finished goods inventory can work well for companies selling lots of identical items, it’s not ideal for a completely bespoke operation. Holding stock of finished goods finished goods accounting inventory means you’re able to shorten customer lead times (compared to made-to-order manufacturing services), but it’s not for everyone. Cost of goods manufactured is the total cost incurred from manufacturing products and preparing them for sale during the current period. There are smaller steps within this process I have excluded for brevity.

The cost of finished goods inventory is considered a short-term asset, since the expectation is that these items will be sold in less than one year. A sample presentation of this aggregated amount of inventory appears in the balance sheet in the following exhibit. The finished goods formula is used to determine the total value of products a company has ready for sale. By looking at key numbers in your production operations, such as direct costs and purchases during the period, you can project how much inventory is available to generate immediate revenue. Code 2817 applies to employers engaged in manufacturing wood products in which woodworking, assembling or finishing operations are performed with power-driven machinery.

By applying the strategies discussed, such as regular audits and demand forecasting, businesses can confidently manage their finished goods inventory and maintain balance in their operations. In this blog, we’ll cover the definition of finished goods inventory, how to calculate it, and best practices for effective inventory management to streamline your business operations. Businesses that actively manage their finished goods inventory can reduce excess stock significantly, leading to improved cash flow and reduced inventory costs.

Imagine transforming your online store from a stockout culprit to an always-in-stock hero, consistently exceeding customer expectations. Ending inventory is the value of the “leftover” inventory that still can be sold at the end of the accounting period. To calculate the ending inventory, we take the total of beginning inventory and net purchases and finish by subtracting the cost of goods sold. Siim Kanne is a production management specialist with more than 15 years of experience in customer-facing roles, sales, onboarding, and technical support.